Quick answer: A houseboat policy must be compared from the actual declarations, endorsements, exclusions, deductibles, insured-value method, navigation terms, and liveaboard conditions. A general boat-insurance description is not proof that a particular houseboat, location, use, or loss is covered.

Houseboat insurance quote worksheet: read the contract behind the price

Ask each insurer to answer these questions in writing for the specific boat, location, primary or occasional use, and navigation plan. Do not treat a marketing summary as the policy.

| Check | What to record | Why it matters |

|---|---|---|

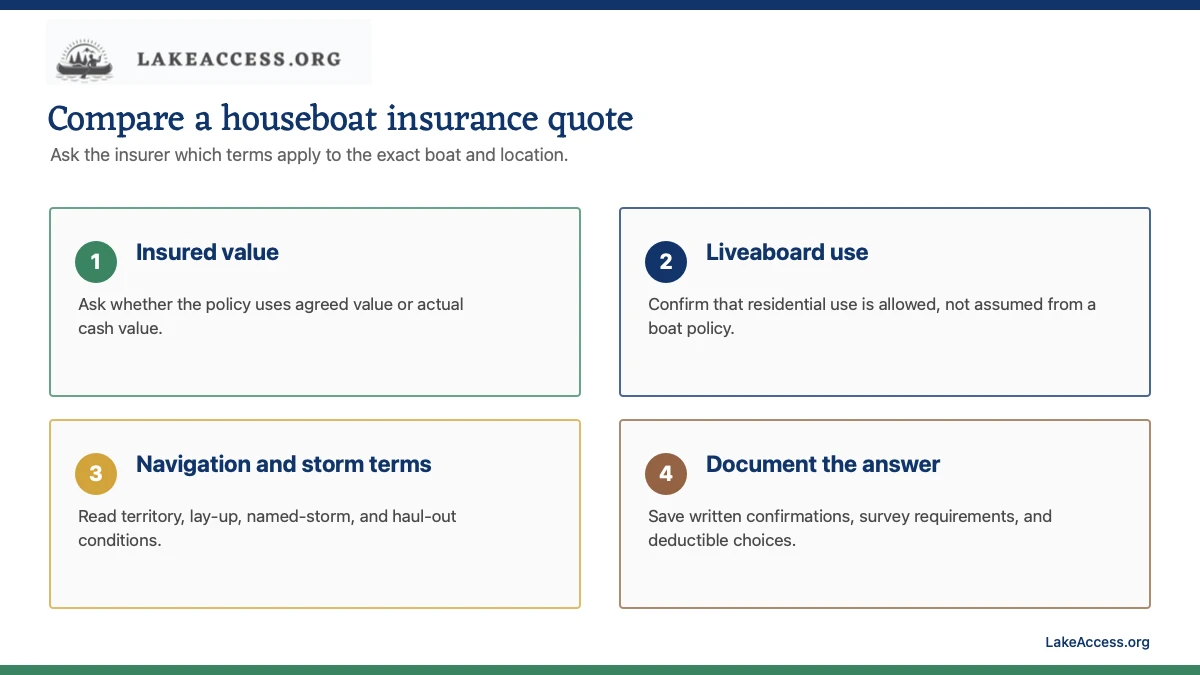

| Insured-value method | Agreed value or actual cash value wording, limits, and depreciation terms | The claim calculation can differ even when the premium looks similar. |

| Use and people | Liveaboard, rental, business, guest, and operator conditions | A boat policy may not treat residential or commercial use the way you expect. |

| Location and weather | Navigation territory, lay-up, named-storm, haul-out, and storage conditions | Coverage can depend on where and when the boat is kept or operated. |

| Claims requirements | Deductible, survey, maintenance, documentation, and reporting duties | A claim question needs the policy terms and the actual facts, not an article. |

Start with the exact boat and intended use

An insurance quote is meaningful only when it describes the actual houseboat and the way it will be used. Provide correct hull, propulsion, age, condition, location, moorage, navigation, and occupancy information. Ask directly whether the insurer treats full-time or part-time residence, a liveaboard arrangement, charter or rental activity, guest use, and storage as covered, excluded, restricted, or subject to an endorsement.

Do not assume that a homeowner, renter, or general boat policy covers a large houseboat because the boat is near a residence or used as one. Consumer guidance from insurance regulators notes that significant boats commonly need separate boat coverage, while the actual policy decides the result. Save the quote, application answers, and written responses so that the coverage decision is based on the same facts that will exist after purchase or a move.

Compare agreed value and actual cash value carefully

Agreed value and actual cash value are not interchangeable labels. An agreed-value structure may set the hull amount when the policy begins, while actual-cash-value language may apply depreciation or market-value treatment. The way partial losses, equipment, machinery, canvases, and personal property are handled can also differ. Ask what values are fixed, what values are adjusted, what proof is needed, and what losses receive a different calculation.

Write the answer beside the amount insured and the deductible. A lower premium may reflect a different valuation method, higher deductible, narrower conditions, or exclusions that matter to the boat. Do not use an article to decide which contract is right for a particular person. Compare like-for-like written terms and take questions about limits, claim handling, or state requirements to a licensed professional or insurance department consumer resource.

Read exclusions and endorsements before relying on the policy

Policies define covered property, covered causes of loss, exclusions, duties, territory, and conditions. A brief quote screen may not display the endorsement that changes a liveaboard, navigation, fuel, sanitation, storm, freeze, mechanical, pollution, or personal-property question. Request the sample form or the applicable policy and endorsements before assuming that a category is included.

Create a list of the features that matter to the planned use: permanent moorage, primary residence, seasonal movement, guests, tender or dinghy, equipment, storm preparation, haul-out, and personal belongings. Ask the insurer to point to the relevant policy section, not merely to say that the boat is insured. Preserve the response with the policy version and effective date because wording can change at renewal.

Check territory, lay-up, and storm conditions

A boat can be subject to navigation territory, seasonal lay-up, storage, hurricane or named-storm procedures, and haul-out terms. These conditions may depend on the boat’s location and the period of the year. They cannot be confirmed by a national guide because the policy, insurer, marina, state, and individual boat condition can all change the answer.

Before changing waters or keeping the houseboat at a new marina, ask whether the policy requires notice, approval, a different deductible, a survey, a plan, or a separate endorsement. Do the same before relying on a seasonal lay-up or assuming that a marina’s storm plan satisfies an insurance condition. The controlling evidence is the current contract and the insurer’s written guidance for the actual situation.

Expect surveys and records to matter

A marine survey, inspection, maintenance history, title or registration record, photos, and service invoices can be relevant to underwriting or a claim. Older boats, unusual construction, prior damage, upgrades, and houseboat systems can increase the need for a current professional assessment. A survey is not a guarantee of condition, but it may identify questions that a quote must address before a purchase or renewal.

Keep a file with the survey, repair recommendations, receipts, manuals, photos, and dated communication with the insurer. If a survey identifies a safety-critical concern, follow the surveyor’s and manufacturer’s guidance rather than treating insurance coverage as permission to defer the work. Documentation also helps distinguish a known condition from a new loss when it is time to ask the insurer how a particular event will be handled.

Use a quote checklist at every renewal

At renewal, compare the boat description, value, location, use, listed equipment, deductibles, territory, exclusions, endorsements, and premium against the prior year. Do not simply renew because the policy number is familiar. A move, new equipment, change in occupancy, repair, different marina rule, or change in navigation can affect whether the current contract reflects reality.

Use the same checklist when accepting an offer on a boat. If coverage depends on a survey, correction, or underwriting approval, place that fact in the purchase and budget plan. This guide is educational, not insurance, financial, or legal advice. A licensed professional and the current policy are the right sources for a coverage decision.

Use this guide as a planning worksheet, not a promise

This houseboat insurance comparison guide explains a repeatable way to collect facts. It cannot determine the terms at a particular marina, the wording of a particular insurance contract, the condition of a particular boat, or a local legal requirement. Those details change by location, season, boat model, operator, and written agreement. Treat any number you find online as a question to verify against a current document rather than a number to copy into a final decision.

Start an evidence sheet with the declarations page, the exact policy form, the boat details, the intended use, and the insurer’s written answers. Add the date, the source, the person or office that supplied it, the period it covers, and the conditions that apply. Keep quotes and rate sheets in the same folder as the worksheet. This makes it much easier to compare like with like and to spot when a monthly price hides a utility charge, a rule, a deductible, a deposit, a condition, or a required inspection.

Separate estimates from obligations

A budget estimate, a vendor description, a manufacturer recommendation, a marina rule, a state requirement, and an insurance contract do different jobs. Put each in its own line instead of treating the most convenient statement as controlling. A planning range can help identify which questions to ask, but it does not authorize occupancy, prove coverage, establish compliance, or certify a system as safe.

When two records disagree, do not solve the conflict by choosing the lower cost or the more favorable interpretation. Ask the organization that owns the rule, service, product, or policy to identify the current controlling document. For electrical, fuel, sanitation, structural, propulsion, or safety-device questions, pause the work and use a licensed insurance professional and, when required, a qualified marine surveyor when the manufacturer instructions or an inspection point to a condition beyond routine owner observation.

Review after a meaningful change

Revisit this worksheet when the boat changes marinas, gains equipment, changes insurers, enters a different season, is used as a residence, or develops a condition that was not part of the original plan. A quote can expire, a dock can change its policies, a renewal can change exclusions, and a utility arrangement can move from included to metered. The old answer may have been sensible for the old situation without applying to the current one.

Keep the source links and a dated summary of the decision. A useful record does not need to predict every cost or failure. It should show what was verified, what was estimated, what remains unknown, and what would cause you to stop and ask a qualified person. That approach is safer and more useful than a generic nationwide answer for a decision that is local and boat-specific.

Compare documents on the same basis

When two quotes or instructions seem to disagree, first check whether they describe the same boat, the same period, the same location, and the same service. A monthly marina price can exclude a resident fee, a policy quote can use a different deductible, and a service recommendation can apply only to a different engine or configuration. Put the assumptions next to each record before deciding that one source is cheaper, broader, or more restrictive.

Use plain labels for each answer: confirmed in a current written document, confirmed verbally and awaiting a document, estimated from a stated method, or unknown. This prevents an estimate from quietly becoming a fact as the plan moves from research to a purchase, a move, a renewal, a repair, or a seasonal change. It also gives the next person an efficient way to check the decisions that are most likely to drift.

Make the next question specific

A useful question names the boat, the use, the location, and the document needed. For example, ask a marina whether this boat can be a full-time liveaboard in this berth under the current agreement, ask an insurer which endorsement applies to this exact use, or ask a service provider which manual section controls this system. Broad questions tend to produce broad answers that cannot safely be carried into a binding decision.

Write down the answer, the person or office, and the date. If the answer changes a cost, safety measure, eligibility, or service plan, update the worksheet immediately. A documented question is also a clean handoff for a surveyor, lender, insurer, marina manager, technician, or family member who needs to understand why a choice was made and what still needs confirmation.

Keep a conservative stop rule

Pause the decision when a required document is missing, a condition is unclear, a quote does not state the intended use, an alarm or visible problem appears, a local rule is uncertain, or a professional identifies work that needs attention. Stopping at that point is not an administrative delay; it is how the plan avoids turning an unresolved assumption into an avoidable cost, claim dispute, compliance problem, or safety incident.

Choose a documented alternative, postpone the step, or obtain the correct inspection or written answer before proceeding. The practical value of a worksheet is not the number of boxes it fills. It is the discipline of showing which answers are dependable, which are provisional, and which decision has to wait for qualified evidence.

Preserve the record for the next review

Save the current documents, not just a summary. Rate sheets, policy forms, manuals, inspection reports, emails, photos, and receipts provide the wording and dates that a later review needs. At the next renewal, move, repair, or seasonal check, compare the new record to the saved one and flag every assumption that has changed before acting on it.

Before you commit

- Confirm the exact boat, location, and liveaboard use on the quote and application.

- Ask how insured value, depreciation, deductibles, machinery, equipment, and personal property are handled.

- Read the policy form and endorsements for exclusions, territory, lay-up, and storm terms.

- Ask whether a survey, inspection, maintenance record, or marina condition is required.

- Retain written answers and recheck coverage before a move, use change, or renewal.

Related LakeAccess guides

- Monthly cost of living on a houseboat

- How much a houseboat costs

- Whether living on a houseboat is legal

- Living on a houseboat year-round

Sources

These sources support the verification questions in this guide. Check the current local rule, rate sheet, manual, and policy before acting.

- NAIC: consumer property-insurance guidance (checked July 15, 2026).

- BoatUS: agreed hull value coverage (checked July 15, 2026).

- BoatUS: line up insurance and financing before an offer (checked July 15, 2026).

- NAIC state insurance department directory (checked July 15, 2026).

- USCG: A Boater’s Guide to Federal Requirements (checked July 15, 2026).